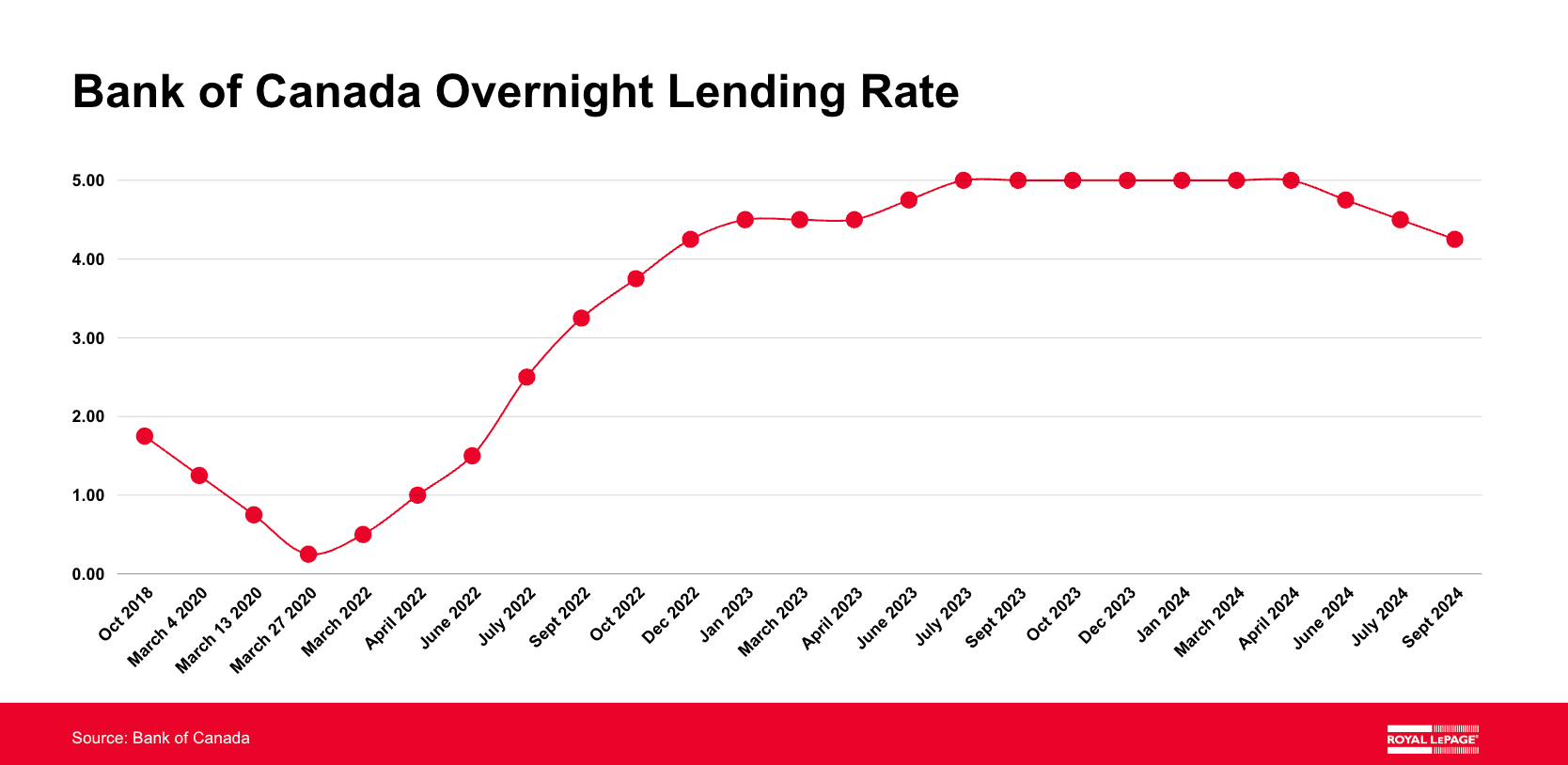

Canada’s central bank has made a third cut to its overnight lending rate this year, lowering borrowing costs for existing and aspiring homebuyers yet again.

In its scheduled September 2024 announcement, the Bank of Canada dropped the target for the overnight lending rate by 25 basis points to 4.25%.

In July, Canada’s Consumer Price Index rose 2.5% year-over-year, increasing at the slowest pace since March 2021. Continued easing of inflationary pressures were a contributing factor of the Bank’s decision to lower interest rates by another 25 basis points.

“Our decision reflects two main considerations. First, headline and core inflation have continued to ease as expected. Second, as inflation gets closer to target, we want to see economic growth pick up to absorb the slack in the economy so inflation returns sustainably to the 2% target. Inflation continues to reflect the push and pull of opposing forces. Overall weakness in the economy continues to pull inflation down. But price pressures in shelter and some other services are holding inflation up,” said Tiff Macklem, Governor of the Bank of Canada, in a press conference with reporters following the announcement.

“If inflation continues to ease broadly in line with our July forecast, it is reasonable to expect further cuts in our policy rate. We will continue to assess the opposing forces on inflation, and take our monetary policy decisions one at a time,” he continued.

Three cuts down – more to go?

The third cut to the overnight lending rate comes at the start of the fall housing market, traditionally a time when buying and selling activity picks up across Canada. For those who have been sitting on the sidelines waiting for cheaper borrowing costs, another decrease to the overnight lending rate may be the extra sign of encouragement they’ve been waiting for.

According to a recent Royal LePage survey, conducted by Leger,1 51% of Canadians who put their home buying plans on hold the last two years said they would return to the market when the Bank of Canada reduced its key lending rate. Eighteen percent said they would wait for a cut of 50 to 100 basis points, and 23% said they’d need to see a cut of more than 100 basis points before considering resuming their search.

For today’s first-time homebuyers who face many financial obstacles on their path to home ownership, lower interest rates mean lower monthly mortgage payments and improved affordability. Another Royal LePage survey, conducted by Hill & Knowlton,2 revealed that three quarters (74%) of those in the next generation of homebuyers – Canadians belonging to the adult generation Z and young millennial cohort, born between 1986 and 2006 – say that owning a home is a priority for them and a milestone they hope to achieve in their lifetime. Buoyed by the prospect of lower borrowing costs, nearly one in five respondents (18%) who are planning to purchase a home say that their timeline to buy is within the next three years, and another 13% plan to buy in three to five years.

“The Bank of Canada continues its delicate balancing act, gradually easing the economic drag of high interest rates as the economy cools. With inflation now at its lowest point in three years, policy-makers are shifting their focus to jobs and housing,” said Phil Soper, president and CEO of Royal LePage. “For first-time homebuyers, the key question is whether to buy now or wait. Home values have largely plateaued this year, and improved affordability due to lower borrowing costs has benefited many. However, once the backlog of sidelined buyers is released into the market, pent-up demand will drive prices higher. This fall, we can expect more cautious Canadians to take the plunge, while those willing to take on the risk might hold out for further rate cuts.”

The Bank of Canada will make its next announcement on Wednesday, October 23rd.

Read the full September 4th report here.